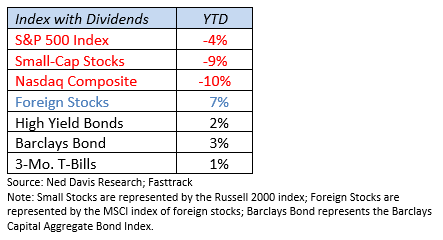

What happened to all the optimism that followed the election? The new administration’s promises of tax cuts and deregulation had many investors hopeful that the bull market would continue for several more years. But as you can see from the table below, reality has been more sobering in the first quarter of the year. Large-cap U.S. companies, especially the technology leaders, posted negative returns.

In addition to the hope for tax reform and deregulation, the new administration introduced another variable—significant tariffs on key trading partners—which has rattled investors and financial markets alike. While the debate continues about the long-term effects of these tariffs on the U.S. consumer and economy, in the short term, investors are clearly interpreting the developments as a net negative.

Unfortunately, inflation hasn’t provided any relief either. Recent data suggest inflation is proving stubborn, remaining above the Fed’s target of 2%. If inflation were to ease back toward that target, it could allow the Federal Reserve to lower short-term interest rates—offering some much-needed support to both stock and bond markets.

Amid the volatility, international stocks offered a bright spot, with broad indices rising nearly 10% in the first quarter. Institutional investors have been eyeing foreign equities for a while now, seeing them as undervalued after years of lagging behind U.S. markets. We’ll see whether that trend holds if tariff tensions escalate further.

Bonds also delivered some welcome stability. High-quality bonds gained nearly 3%, a refreshing change after years of underwhelming performance. High-yield bonds eked out a slight gain, though they remain somewhat tethered to stock market movements.

How We’re Responding

From the S&P 500’s peak on February 19 to its low on March 13, the index dropped 10%, while small-cap stocks and the Nasdaq index saw closer to 15% declines. This kind of pullback activated our FSA Safety Nets®—our exit system designed to limit portfolio risk in periods of sustained market weakness. All our actively managed strategies have increased their allocations to money market funds as a result. While it’s still too early to determine whether the overall trend in U.S. equities has turned definitively downward, the markets are certainly at a tipping point. Time will provide additional clarity that either reinforces a more defensive stance—or signals the opportunity to redeploy some of the money market allocations.

What May Lie Ahead?

Beyond the immediate concern regarding tariffs, there is a larger issue looming: the growing risk of recession. The primary measure of economic growth—GDP—has slipped from 3% growth in the second quarter of 2024 to a forecast of 0.3% for the first quarter of this year. That decline is getting us dangerously close to contraction, and two consecutive quarters of negative GDP growth would meet the technical definition of recession.

The Leading Economic Index has also been trending lower for several years, a pattern that has historically preceded recessions. However, employment remains robust, and job growth is still solid, making the outlook more complex. If tariffs persist or expand, the pressure on the economy could increase, reinforcing the case for a slowdown.

That’s why now, more than ever, it’s essential to have a flexible and active investment process—one that can respond dynamically to changing conditions, instead of relying on static allocations or hope.

At FSA, we’re not just monitoring the markets—we’re actively managing your portfolio with discipline and care. While we can’t eliminate market volatility, we can help you navigate it with a structured plan, a calm hand, and a focus on your long-term goals.

If you’re feeling uneasy or would like to talk through recent developments, don’t hesitate to reach out. We’re here for you.

Portfolio Update

Keep in mind that because we manage clients’ portfolios individually, the holdings in your specific accounts may differ somewhat from the averages.

Strategies That Employ the FSA Safety Net®

Income (Strategy 1)

As mentioned above, both high-quality and high-yield bonds managed to gain ground in the first quarter. As quality bonds began to recover early this year, we added 15% to those types of funds. It has been a choppy ride with these types of funds over the past few years, so we are hesitant to increase our allocation here until there is further confirmation of an uptrend. Currently, portfolios hold 40% in high-yield bond funds, 15% in high-quality funds, and 40% in more eclectic and defensive bond funds.

Income & Growth (Strategy 2)

This strategy is managed very defensively, quick to build up a money market allocation if stocks or bonds weaken. At the beginning of the year, this strategy was 50% in equities, but that has been reduced to 25% more defensive equity funds. The bond allocation increased from 40% to 58%. The money market allocation has increased to 17% of the portfolio. There is 10% in money markets, the majority of that allocation in the higher yielding Schwab Value Advantage.

Conservative Growth (Strategy 3)

Clients in our Conservative Growth strategy saw their equity allocation drop from 75% to 45% in Q1. In addition to the 20% allocation to high-yield bonds, we added a high-quality bond fund, bringing the fixed allocation up to 30%, leaving 25% in money market funds, primarily Schwab Value Advantage.

Core Equity (Strategy 4)

Core Equity accounts have essentially tracked the movements of the S&P 500 this year. As funds have hit the FSA Safety Net®, however, we have been building up the money market allocation. So far, these funds have been large-cap growth-oriented funds, since they have been hit the hardest in this decline. The current asset allocation is 75% equities and 25% money markets.

Tactical Growth (Strategy 5)

Befitting our most aggressive strategy that employs the FSA Safety Net®, it remains with a healthy allocation to equities at 80%. We did jettison a few of the more growth-oriented holdings and added some international exposure. These portfolios hold 20% in money market funds.

Active Strategies WITHOUT the FSA Safety Net®

Sector Rotation

Market turmoil has buffeted this strategy which only trades sector funds. For the most part it has risen and fallen with the S&P 500 index this year. In the March rotation the strategy picked up the inverse fund which can act as a cushion when stocks fall. Currently, the portfolio contains energy, basic materials, health care, financial services, and the inverse fund.

Global Rotation

In 2024 this strategy rode technology train and posted solid returns. This year, with technology stocks struggling, this strategy suffered. During the quarter, we sold two of the mid-cap funds and added two funds with foreign exposure and sold one of the large-cap growth funds to the money market. The current portfolio includes roughly 50% in U.S. large-cap funds, 30% in global/foreign funds, and 20% in money market funds.

Strategies That Remain Fully Invested Through ALL Market Cycles

Global Balanced

It was good to see this more conservative passive strategy fare relatively well in this difficult first quarter. Obviously, the high allocation to bonds helped, as did the allocation to international stocks and even real estate.

Global Moderate

This strategy managed to post a positive return for the year, with its broad allocation to various assets providing both a cushion to the losses in the U.S. market, as well as a boost to its returns. International stocks and an allocation to gold provided the biggest boost to returns.

Global Growth

This aggressive strategy holds 90% in stocks, but held up quite well in the first quarter, thanks to its diversification among asset classes. International stocks and gold provided the best help to returns while small-cap stocks were the biggest drag on returns.

Please remember to inform your advisor of any changes in your life that might affect your investment objectives and how we manage your money.

Ronald Rough, CFA

Chief Investment Officer

Disclosures are available at www.fsawealthpartners.com/disclosures/market-update.

FSA’s current written Disclosure Brochure and Privacy Notice discussing our current advisory services and fees is available at www.fsawealthpartners.com/disclosures or by calling 301-949-7300.