By Mike Zarrelli, CFP®, EA

Investing is not a one-size-fits-all approach. As markets shift, different strategies excel in different environments. At FSA Wealth Partners, we believe in the power of active management, but we also recognize the value of passive investing. The key is understanding when and how to use each strategy to maximize long-term wealth while managing risk and tax efficiency.

Understanding Active vs. Passive Investing

Passive Investing: This strategy follows a “buy and hold” approach, often through index funds or ETFs that track market benchmarks like the S&P 500. It works well in strong, secular bull markets, where broad market growth lifts all investments—a rising tide raises all ships! Passive investing is typically low-cost and tax-efficient but lacks downside protection in volatile or declining markets.

Active Investing: This approach involves adjusting portfolios based on market conditions, economic data, and risk assessments. Our proprietary FSA Safety Net® strategy is designed to protect portfolios in bear or stagnant markets while allowing participation in growth periods—make hay while the sun is shining! Active management thrives during periods of market uncertainty, flat growth, or downturns, where a hands-on approach can reduce losses and seize opportunities.

When Each Strategy Works Best

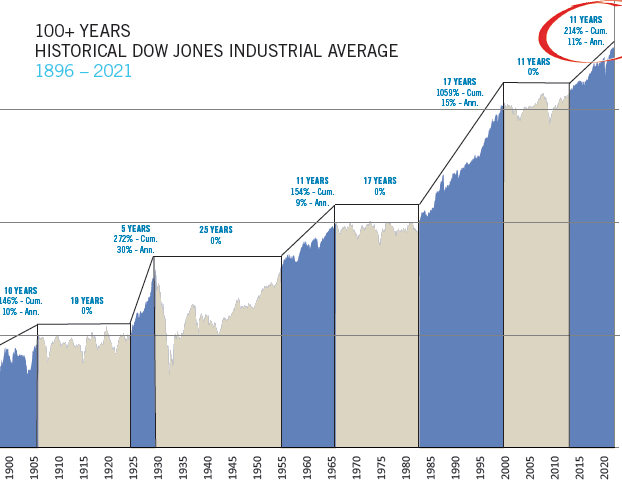

Using historical data, we can see how market conditions favor different strategies:

- Passive investing shines in bull markets: When markets experience long-term growth (bull markets such as the roaring ’20s, the 1990s, or the 2010s), passive strategies tend to perform well due to broad market participation and compounding returns. These are the blue periods in the chart below.

- Active investing excels in volatile or stagnant markets: During downturns (like the stagflation era, the dot-com bubble, and the Great Financial Crisis), actively managed portfolios with risk mitigation strategies, such as the FSA Safety Net®, helped investors avoid steep losses and preserve capital. These are the tan periods in the chart below.

How They Work Together: A Balanced Approach

Rather than choosing one approach over the other, blending active and passive strategies can optimize risk and return:

- Active management provides risk control: Reducing downside exposure can shield long-term wealth. It makes the bear markets less scary!

- Passive investing captures long-term market growth: Keeping costs low and staying invested in bull markets maximizes compounding returns. This is great for your long-term buckets of money!

- Liquidity and flexibility: Passive investments provide a strong foundation for long-term growth, while active management can adjust to changing market conditions in real time. By having both strategies in your portfolio, you can have your cake and eat it too. Money in your portfolio that is earmarked for short- to medium-term goals, such as retirement living expenses for the next five years, may be better suited in an active risk management approach; whereas money that won’t be touched for decades has more time to ride the waves of the stock market.

Tax-Efficient Investing and Portfolio Construction

One important consideration when balancing active and passive strategies is tax efficiency. Active trading can generate taxable gains in taxable investment accounts, particularly short-term capital gains, which are taxed at your income tax rate. In contrast, long-term capital gains are taxed at preferred capital gains rates, typically 15% for most folks. While our FSA Safety Net® strategy is tax-aware (we do our best to hold on to positions for at least a year), the first and foremost priority of the strategy is to protect on the downside.

Passive investments, with lower turnover, typically generate fewer taxable events. Strategies like tax-loss harvesting (we’ll talk more about this later) and investing in tax-efficient funds can help reduce your overall tax burden.

So, how can you use both strategies in tandem without increasing your tax bill? By using proper investment strategy location. This means placing less tax-efficient strategies in tax-advantaged accounts (like IRAs and 401(k)s) and utilizing passive investments in your taxable investment accounts.

For example, placing our Core Equity Safety Net Strategy in tax-advantaged accounts like IRAs or 401(k)s can shield the short-term trades from immediate taxation, while placing our Global Moderate passive strategy in taxable accounts can minimize capital gains taxes over time.

FSA’s Approach to Investment Management

At FSA Wealth Partners, we employ both strategies to create a well-rounded portfolio tailored to each client’s goals. Our active management, powered by the FSA Safety Net®, is designed to safeguard portfolios when markets turn, while our passive investment options provide long-term, tax-efficient growth opportunities.

Additionally, we incorporate strategies such as:

- Rebalancing portfolios regularly to maintain the desired mix of active and passive investments.

- Tax-loss harvesting to unload investments that may be carrying a capital loss to offset other holdings that might be sold at a taxable gain.

- Roth conversions to potentially reduce your lifetime tax bill and provide opportunities for tax free growth!

- Using tax-efficient withdrawal strategies to optimize distributions in retirement.

- Monitoring economic conditions to make adjustments that align with market shifts.

Final Thoughts

Investing is not just about maximizing returns, otherwise, every investor would be invested 100% in stocks. Rather, investing is a balance of generating growth, preserving wealth, and pursuing financial stability through all market cycles. By leveraging both active and passive strategies, investors can create a resilient portfolio.

Together, we create an investment plan that matches your needs, so you can spend more time enjoying the fruits of your labor. To schedule a meeting, call (301) 949-7300 or email [email protected].

About Mike

Mike Zarrelli, CFP®, EA, is a Financial Advisor at FSA Wealth Partners (FSA). Since joining FSA in November 2018, Mike has provided clients with personalized financial and retirement planning, using his passion for simplifying complex financial topics to empower informed decision-making. Working closely with senior advisors, Mike helps clients optimize their finances, avoid nasty money mistakes, and ultimately enjoy their wealth today and tomorrow.

Mike studied personal finance and accounting at Salisbury University. During his time in school, he was actively involved in the Financial Management Association and served as treasurer of his fraternity, Pi Lambda Phi. He holds the CERTIFIED FINANCIAL PLANNER® and Enrolled Agent (EA) designations and is a member of the Financial Planning Association.

Before FSA, Mike gained client-first experience at PNC Financial Services as a bank teller, where he learned the importance of prioritizing client needs, and as a server, which strengthened his commitment to exceptional customer service.

Outside of work, Mike is an outgoing family man who finds joy in spending time with loved ones, relaxing at the beach, and renovating his house. He’s also an avid sports fan (Go Commanders!), touch rugby player, golfer, and enjoys staying active by working out.

You can connect with Mike on LinkedIn here.

FSA’s current written Disclosure Brochure and Privacy Notice discussing our current advisory services and fees is also available at https://fsainvest.com/disclosures/ or by calling 301-949-7300.

The FSA Safety Net, a registered differentiator, effectively highlights our investment management approach. However, it has been used in contexts related to financial planning, where its relevance is less clear. To ensure clarity and alignment, we propose developing a complementary tagline specifically for the financial planning side of our services. This could pair with the FSA Safety Net, such as “The FSA True Wealth Process,” to clearly differentiate our comprehensive planning solutions. The goal is to create cohesive messaging while reinforcing the distinct value of each service area.