And just like that, 2024 is in the books. This year, like many others, brought its share of ups and downs, wins and losses, and lessons learned. Each year, major news stories shape the way we think about the future. These stories can span the economy, politics, and even company-specific news. Today, we’ll look back at some of the biggest financial moments of 2024 and explore how they might affect your wallet moving forward.

Inflation vs. Interest Rates – the Story Continues

Inflation can make buying everyday goods tricky. How do you combat inflation? With interest rates. Inflation peaked near 9% in 2022, prompting the Federal Reserve (FED) to raise interest rates 11 times. Why does raising rates slow the economy? Simply put, increasing borrowing costs discourages spending, decreases money in circulation, and dampens the economy.

By 2024, inflation had cooled, leading the FED to reverse course with three rate cuts. Why does lowering interest rates help the economy? Simply put, reducing borrowing costs encourages spending, increases money in circulation, and stimulates economic activity.

What does this mean for you?

- Mortgage Rates: Despite the cuts, mortgage rates remain around 7%, and housing prices are still high. If you’re planning to buy a home in 2025, prepare for continued challenges.

- Savings Accounts: High-yield savings accounts and money market funds are paying 3.5%-4%, so make sure your cash earmarked for short-term goals is working for you.

- Long-Term Goals: Stick to your investment plan (if your goals or life circumstances haven’t changed). Rates go down, rates go up, but this remains true: the stock market is an amazing long-term wealth building tool.

A New President in the White House

A change in leadership often stirs uncertainty, with one side celebrating and the other fearing the future. But here’s the truth: when you zoom out, the stock market doesn’t really care who’s in the Oval Office.

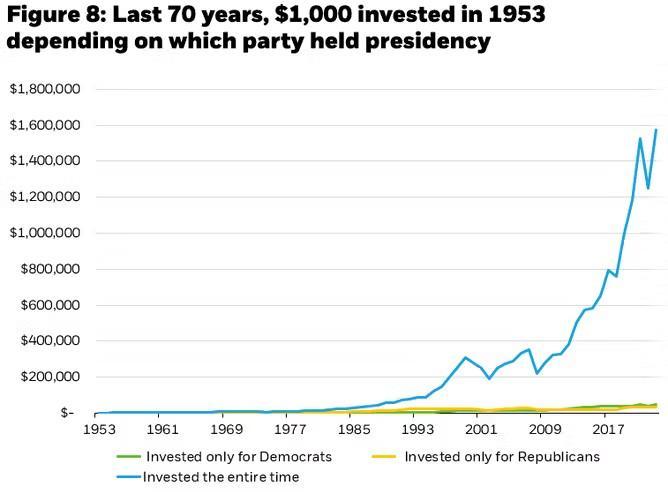

Historical data shows that staying invested regardless of political changes is key. From 1953 to today, $1,000 invested in the S&P 500 would have grown to $1.6 million if you stayed in the market through every administration. On the flip side, investing only when a specific party was in office would leave you with far less—around $200,000. These investment decisions can be the difference between retiring early versus working several extra years.

What does this mean for you?

The stock market’s long-term growth is driven by factors like company earnings, innovation, and economic conditions—not political shifts. Businesses adapt to new rules and policies, ensuring they remain profitable and keep the economy growing. Again, it is prudent to stick with your investment plan. Remember: investing is emotional, but investing based on emotions tends not to be a great strategy.

The AI and Crypto Boom!

Tech (unsurprisingly) took center stage in 2024. Nvidia’s stock soared over 170%, while Bitcoin surpassed $100,000 for the first time ever!

AI continued to be a buzzword, with over 40% of S&P 500 companies mentioning it during Q2 earnings calls. Meanwhile, crypto received a boost from the launch of the first Bitcoin ETF and Trump’s pro-crypto campaign.

With huge gains in 2024, the big question is: Should you invest in it now? My counter question is if AI stocks and crypto didn’t grab your attention at the beginning of the year when Nvidia was trading at $52/share and Bitcoin was near $40K/coin, what’s different now?

There’s certainly a place for speculative investments in some portfolios, especially if you already have a high savings rate and plenty of boring, old, diversified index funds (the tried and true way to building wealth). The worry here is that folks may jump blindly into speculative investments based on past returns, social media hype, or FOMO. This is generally a risky move!

Here’s how to approach speculative investments:

- First, do your research to get an understanding of the investment and build your conviction. The goal is to either confidently answer why this investment will continue to go up or decide it’s not the right fit for you!

- Then, determine how much you’re willing to risk & create an investment plan to allocate your funds — you could earmark 1%-5% of your portfolio for speculative investments, then decide whether to invest in a lump sum or through dollar-cost averaging.

- This next step is super important…know what you’re aiming for. If your speculative bucket doesn’t have a goal tied to it, how will you know when to sell or trim the investment if your conviction was right? This could be to pay off your mortgage, retire early, or seed money to start your dream business.

- Lastly, be ready to hold on for dear life. It’s going to be a volatile ride!

What does this mean for you?

FOMO, Emotion, and Greed are not real investment strategies. Do your research, create a plan, define your goal, & be ready for a bumpy ride.

Final Thoughts

When you zoom in on any year, there are always reasons to worry—wars, recessions, political drama, etc. But there’s one common truth – panicking has never been a smart strategy. A solid financial plan, combined with flexibility and liquidity, is the best way to face uncertainty.

Heading into the new year, we have two choices:

- Focus on the things we CAN’T control, like market returns, geopolitical issues, or the news cycle.

- Or focus on the things we CAN control, like your income, spending, savings rate, being kind to others, and making memories with loved ones!

At FSA, we help you prepare for the unknown so you can sleep well at night. If this blog resonates with you, email us at Questions@fsawealthpartners.com or call 301-949-7300 to connect with one of our CERTIFIED FINANCIAL PLANNER® professionals. See you in the next post!

FSA’s current written Disclosure Brochure and Privacy Notice discussing our current advisory services and fees is available at www.fsawealthpartners.com/disclosures or by calling 301-949-7300.